We expect increasing demand for level measurement and inventory tank gauging technologies as companies use these tools to improve operational efficiencies, increase productivity, gain greater control over inventories, and achieve enhanced accuracy. VDC is forecasting a 5.2% CAGR through 2016, reflecting total shipments of almost $3.3 billion, comprising thirty-four different technology segments (shown in the table in Figure 1).

Figure 1. Technology segments for process level measurement and inventory tank gauging

| Electronic Process Level Measurement | Mechanical Process Level Measurement | Electronic Inventory Tank Gauging | Mechanical Inventory Tank Gauging |

| Capacitance/RF admittance | Diaphragm | Capacitance/RF admittance | Float (single-point) |

| Conductive | Displacer | Hydrostatic Tank Gauging | Float (multipoint) |

| Hydrostatic pressure | Float (single-point) | Magnetostrictive | Float and tape |

| Laser | Float (multipoint) | Radar (noncontact) marine | Paddlewheel |

| Load Cell | Hydrostatic pressure | Radar (noncontact) non-marine | Weight and cable |

| Magnetostrictive | Paddlewheel | Radar (contact) | |

| Microwave/Radar (noncontact) | Tilt | Sonic/ultrasonic | |

| Microwave/Radar (contact) | Weight and cable | Servo | |

| Nuclear | |||

| Optical | |||

| Sonic/Ultrasonic | |||

| Thermal | |||

| Vibration |

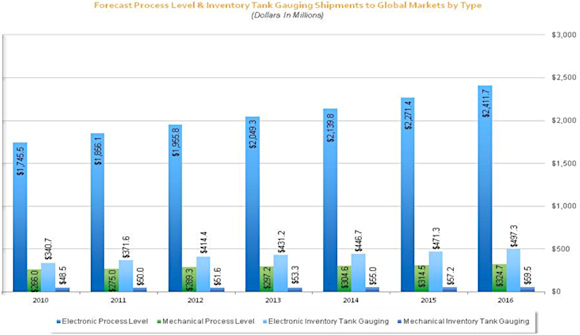

Of the $3.3 billion market opportunity, more than 88% represents electronic process level measurement and inventory tank gauging systems, of which electronic process level devices will make up 83% of that 88% share (Figure 2). Feedback received by VDC indicates that users are increasing their reliance on electronic process level and tank gauging systems to provide access to real-time information, typically connected to IP-based networks via a fieldbus or Ethernet application-layer network protocol, and thereby enabling greater automation, flexibility, and agility in operations and/or greater accuracy for custody transfer and inventory storage and control.

Figure 2. Forecast process level and inventory tank gauging shipments to global markets, by type, dollars in millions (Click image for larger version) |

Within the process level measurement market, shipments of continuous level measurement devices will remain more than 3.3 times larger, on a dollar volume basis, than those for point measurement devices despite the fact that the market for point measurement devices is experiencing faster growth, driven by the increased need for safety systems and overfill protection. Continuous level measurement is required in a larger number of applications and the devices used to serve those applications are far more expensive than point level devices.

For those devices that include network connectivity, users are relying on a number of different wired network interfaces, including HART, Modbus, Profibus, and Foundation Fieldbus, to provide real-time data for greater flexibility, operational agility, and actionable information in decision-making. A growing number of users are increasing their reliance on wireless networks such as Wireless HART because of the resulting reduction in cable costs and maintenance, increase in mobility and flexibility, ability to operate in areas previously not accessible via cables, greater scalability, and ease of installation. Within the electronic process level measurement technology market, the largest share of shipments—more than 33% in 2016—will be for hydrostatic pressure transmitters, despite the robust growth in the use of microwave/radar (contact and noncontact) devices. The persistent dominance of hydrostatic level sensing can be attributed to a number of considerations, such as low product and/or maintenance cost, ease of installation, ruggedness, proven reliability, broad media compatibility, as well as user familiarity.

Regardless of the attributes that matter most to the end user, for a new level sensing technology to gain significant traction, it must optimize the mix of price, performance, and operation to offer a credible alternative to the venerable hydrostatic level sensor in an array of mainstream applications. The prevailing strategy of targeting only those applications where hydrostatic sensors don't work is both limiting and shortsighted. A microwave/radar level gauge as a drop-in replacement for a side-mounted hydrostatic level transmitter is not feasible, but it should be possible to achieve some degree of equivalency for other key characteristics. Hydrostatic level sensor emulation should be a priority for any supplier seeking to realize greater success in the process level marketplace.

Noncontact, microwave/radar marine and non-marine inventory tank gauging systems form the bulk of the electronic inventory tank gauging market, representing almost 59% of the overall total in 2011. Demand for these radar devices, which are perceived to offer greater performance and higher accuracy, is expected to drive their share to 61% of the overall electronic tank gauging market by 2016. Demand for the radar units designed for use in non-marine tank gauging applications will be more robust because these units typically have much lower price points and can serve a broader range of applications.

Among the smaller market for mechanical process level measurement devices, the predominant technologies used are displacer transmitters and single-point float switches; combined, we expect these devices to represent almost 81% of the slower-moving mechanical market in 2016. Benefits of displacer sensing include simple control capability, easy set-point change, and the fact that the technology is well established in the gas and petroleum market. Its disadvantages include the fact that it can only be used for nonfreezing liquids, calibration is difficult, and it is susceptible to changes in specific gravity. Single-point float switches will remain the second most demanded mechanical system used because of the technology's simplicity, lower price points, and ease of use. The market for multipoint float switches is growing but is expected to remain a fraction of the market, despite greater performance and product improvements.

Among the smallest markets for mechanical inventory tank gauging (ITG), the dominant technology will continue to be single-point float ITG devices. Rising oil prices are driving increased investment in oil and gas exploration and production, which in turn requires more storage and greater inventory gauging accuracy, especially for custody transfer applications. The marine segments (which mainly involve transporting gas and/or petroleum) and the gas and petroleum segments combined represent more than 74% of overall shipments. Single-point float ITG devices will remain the dominant choice due to their adequate accuracy, lower costs, ease of use, and user familiarity.

Many end-user markets use one or more of the thirty-four process level measurement and/or inventory tank gauging technologies under study. Figure 3 lists the industries that consume these technologies, based on 2011 dollar volume shipments and ranked from highest to lowest consumption.

Figure 3. The largest consumers of process level measurement and/or inventory tank gauging systems, ranked in descending order

| Electronic Process Level Measurement | Mechanical Process Level Measurement | Electronic Inventory Tank Gauging | Mechanical Inventory Tank Gauging |

| Gas and petroleum (including refineries) | Gas and petroleum (including refineries) | Gas and petroleum (including refineries) | Marine |

| Chemical | Electric power | Marine | Gas and petroleum (including refineries) |

| Water/wastewater | Chemical | Petrochemical | Food and beverage |

| Electric power | Food and beverage | Chemical | Chemical |

| Petrochemical | Petrochemical | Electric power | Petrochemical |

| Food and beverage | Marine | Food and beverage | Electric power |

| Pharmaceutical | Water/wastewater | Water/wastewater | Water/wastewater |

| Marine | Plastics | Pharmaceutical | Pulp and paper |

| Aggregates | Aggregates | Pulp and paper | |

| Mining | Pharmaceutical |

VDC has determined that certain technologies are better suited for particular applications, based on factors such as environmental operating conditions (e.g., harsh or hazardous environments), price/performance, accuracy requirements, and network connectivity requirements. For example, a supplier of a noncontact microwave/radar device will be less likely to market this technology for water/wastewater applications because these are more likely to already be using hydrostatic and/or sonic/ultrasonic systems. The majority of devices used in marine applications were likely used in shipping gas and petroleum; combined, the marine and water/wastewater segments represent the bulk of inventory tank gauging system shipments.

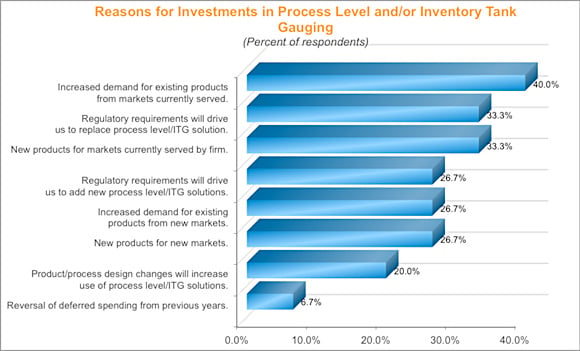

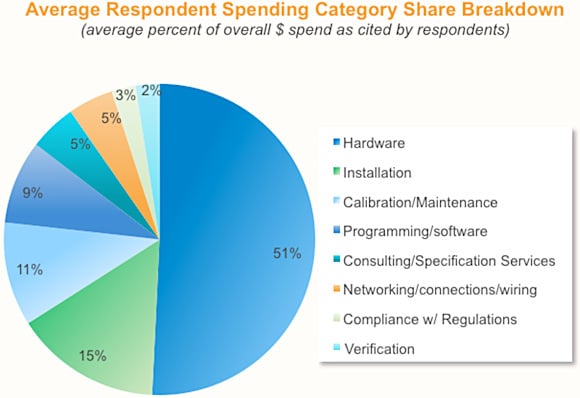

The chart in Figure 4 represents a breakdown of feedback from 340 respondents listing the key factors that drive their increased investment in future process level measurement and/or inventory tank gauging systems. The process level measurement device and/or inventory tank gauging system being sold is only one factor among many that are considered when most end-user organizations select a process level measurement or ITG system (Figure 5). Given that electronic devices make up the bulk of the market, suppliers should focus on developing either best-in-class in-house application and technical support capabilities or they should partner with third parties who possess the requisite technical expertise, applications knowledge, and strong customer service programs.

Figure 4. Reasons for investments in process level and/or inventory tank gauging |

Figure 5. The breakdown of the average respondent's spending, listed by category (numbers represent the average percentage of overall money spent as cited by the respondents) |

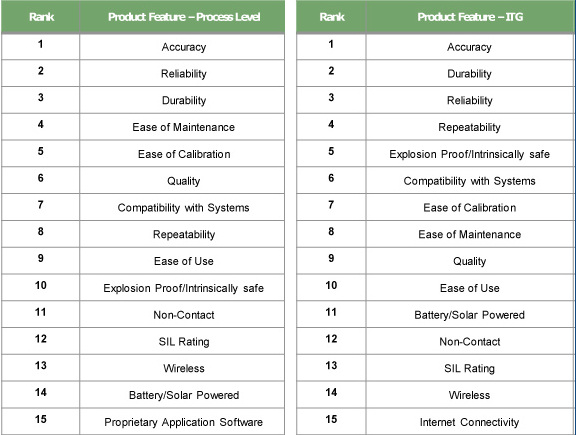

When the respondents were asked to list the most important product features considered when investing in a process level measurement or ITG system, accuracy topped the list. Figure 6 lists the respondents' top 15 product features, ranked from most important to least important.

Figure 6. The top fifteen product features for process level (left) and inventory tank gauging (right) |

Respondents indicated that they wanted/needed suppliers who can provide best-in-class product features and performance, but that they also required the suppliers to provide the following: reliable product availability with timely delivery; local or on-site technical and product support; spares, free product demos, a broad product selection, and long-term product support. A supplier's reputation and brand name recognition are also important to the respondents.

Within the markets for process level measurement and ITG The competitive landscape is almost as fragmented as the number of different technologies that make up the process level and ITG ecosystems. VDC found that the market for these technologies is being served by large and small companies, by companies with relatively broad technology and product portfolios as well as companies with focused product portfolios consisting of a single technology and/or product. In most cases VDC determined that the companies that offer the broader (or broadest) technology offerings, supported by strong service and support (whether provided in-house or via third-party partners) enjoyed the greatest success in terms of market-share gains and overall sales volumes.

Figure 7 lists the leading suppliers of the respective technology segments, based on 2011 worldwide dollar volume shipments, and ranked in descending order.

| Electronic Process Level Measurement | Mechanical Process Level Measurement | Electronic Inventory Tank Gauging | Mechanical Inventory Tank Gauging |

| Endress + Hauser | Magnetrol International | Emerson (Rosemount/Saab) | Musasino |

| Emerson (Fisher/Rosemount/Mobrey) | Emerson (Fisher/Rosemount/ Mobrey) | Honeywell Enraf | BinMaster |

| Vega | Dresser-Masoneilan (GE) | Invensys | Varec |

| Yokogawa | Invensys | Kongsberg Marine | Invensys |

| Siemens | Tokyo Keiso Co. | Robertshaw Industrial Products | Robertshaw Industrial Products |

| ABB (K-TEK) | UWT GmbH | Musasino | L&J Engineering |

| Magnetrol | Schneider Electric (Square D) | Endress + Hauser | Thermo Fisher Scientific |

| Invensys | Kimray | Gauging Systems | Motherwell Tank Gauging |

| Vishay Precision Group | SOR, Inc. | Tokyo Keiso Co. LTD | Franklin Fueling Systems |

| Ametek Drexelbrook | Venture Measurement | Cameron | (Barton) |

Figure 7. Leading suppliers ranked in descending order

In the final analysis, VDC determined that the greatest opportunity for vendors lies in supplying a relatively broad base of electronic process level measurement and/or inventory tank gauging systems. For suppliers that lack the size, financial backing, and necessary resources to provide a broader product portfolio, VDC recommends that suppliers focus their efforts on serving niche market application segments with the technologies that are best suited to meet those specialized application requirements.

Companies will always need to measure their process operations and/or manage their inventory, so the market outlook is fairly robust as a whole and represents a growth area for electronic solutions that enable network connectivity and access to real-time information. Companies are increasingly seeking out suppliers for partnerships; looking for suppliers that are focused on helping the customer to better compete in their own business.

ABOUT THE AUTHOR

J Timothy Shea is a Senior Analyst at VDC Research Group, Natick, MA. He can be reached at 508-653-9000, x-132, or [email protected].