Collaborating with Vision Systems Design and Inspect trade journals, imaging company FRAMOS delivers its tenth market study that identifies criticl trends in the industrial cameras industry based on user and manufacturers views. This year of 2017, the study consists of 90 manufacturers and users from 22 countries responding to questions about the state of the imaging market and its future development.

In the Age of Automation and the Smart Factory, classic machine vision is the cornerstone of success for the Imaging industry. CMOS technology and fast processing are enabling real-time precision, while cognitive vision solutions using artificial intelligence are the bases for further growth. Customized embedded vision is expanding into a wider range of industries and innovative applications, boosting their performance and efficiency. Integrated image processing, which provides a combination of reliability, superior quality, and a high level of innovation, is now a basic building block in the digitally networked world.

This study is based on opinions from 61 users and 29 manufacturers who gave comprehensive information about the imaging market, cameras, sensors, applications and trends. European respondents, at 68%, were the largest responding group, while North Americans accounted for 19% with the rest coming from Asia and The Middle East, at 13%. Relevance ranking was carried out based on purchase or production volumes. Purchase and production were concentrated in Europe, at 61% and 50%, respectively. Also, manufacturers built more products in both Asia (24%) and North America (24%), signaling an increase in these two regions compared to previous years. The Asian and North American purchasing trends rank behind Europe, accounting for 31% and 8% of users, respectively. The Asian purchase market declined compared to last year (28%), partly because there were fewer survey participants from Asia, but these figures also suggest that the European and North American markets are stabilizing (See Chart 1).

A Market Based on Machine Vision, with Artificial Intelligence for Innovative Systems

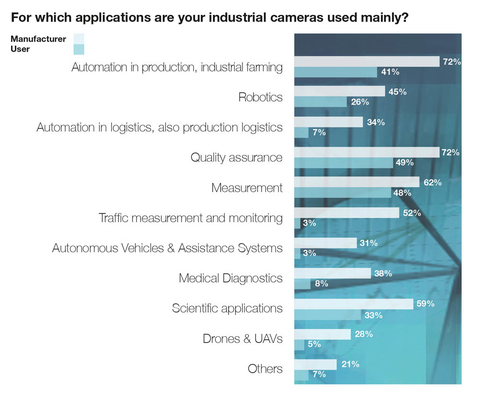

Automation in production and agriculture, like in previous years, is the main imaging field according to both manufacturers and users. Quality assurance is the top camera application for both manufacturers (72%) and users (49%), followed by opto-sensory measurement tasks (62% and 48%, for manufacturers and users, respectively). Also, robotics and scientific applications still represent an important part in the total imaging sales and purchase decisions, as outlined by the responders of this survey. Manufacturers reported 115% growth in the transportation sector compared to 2016, driven by autonomous vehicles and assistance systems applications.

Meanwhile, medical technology was stagnant and did not grow in 2017. The fact that machine vision is expanding into more fields shows that manufacturers are capitalizing on the huge potential of innovative technologies: 28% of respondents stated that their cameras are used for drones and unmanned aerial vehicles (UAVs). Other application areas that are seeing increases include those based on artificial intelligence, 3D scanning, gesture control, and virtual reality. While users recognize this potential, they are still firmly focused on traditional machine vision applications (See Chart 2).

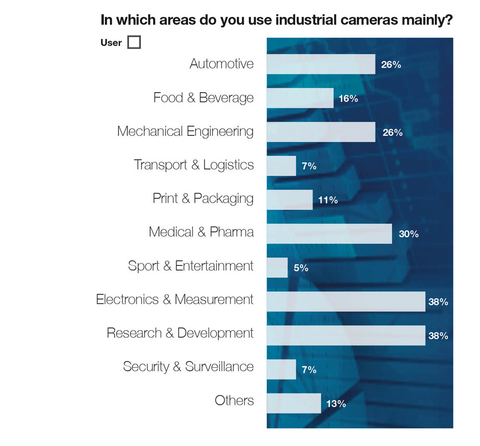

At the industrial level, electronics, mechanical engineering and measurement technology continue to dominate both production and sales; in fact, they increased their lead slightly compared to 2016. The automotive industry remains a key player, albeit with a 17% drop compared to last year. Users and manufacturers agree on the importance of the R&D sector, including the medical and pharmaceutical fields, which retained their positions in the ranking. Other significant verticals for manufacturers are the food and beverage, print and packaging, security and surveillance, and, logistics. A growth area identified by manufacturers includes the multimedia and entertainment markets.

Generally, manufacturers who respond naturally cover a broader range of applications and industries than do users, who tend to be concentrated in certain markets. Manufacturers are more innovation-driven, while users are more focused on traditional vision applications.

Sustained Investment Confidence, Embedded Vision, and Possible Market Fragmentation

Camera manufacturers' main customers are OEMs and system suppliers who make up 39% of their customer base – an increase of 30% compared to 2016. This increase underlines how the imaging market is moving toward embedded vision with more complex systems and requirements. Consequently, end users are becoming less significant (-63%), but this trend is largely offset by increased sales by distributors acting as intermediaries and consulting vision experts. System integrators remain a stable customer segment at 31%.

Both trends clearly show that users are looking to the technical expertise of external partners to develop their integrated systems. Fifty-seven percent (57%) of users stated their vision systems were developed and implemented in-house, however, this is a declining trend – shown by an 11% drop from last year – which infers that they are more likely to seek support from value added distributors more often in the coming years. Twenty-four percent (24%) bought a complete system (a 9% increase) with only 13% supported by a system integrator.

Given this increase, the proportion of system integrators remained consistent at 54%. This is significant in terms of the role that intermediaries and experts are playing between manufacturers and end users.

Manufacturers predict strong and secure ongoing growth in the machine vision industry. Thirty-eight percent (38%) expect this growth to be driven by new users; 21% by the modernization of existing systems; and, 41% by customers who require a mix of the two.

Manufacturers see artificial intelligence, 3D imaging, hyperspectral imaging, and embedded vision as key drivers; and, 21% of manufacturers see embedded vison as an opportunity to grow further. Most users (91%), plan to continue investing in imaging with 52% of them intending to introduce either new or modernized vision systems over the next two years, while another 39% anticipate doing a mix both types of investment. In line with the users in more traditional application fields and industries, 75% stated they would be using off-the-shelf (OTS) components with 39% of all user respondents stating they would like to develop their own solutions.

This result outlines what manufacturers see as the risks of traditional machine vision markets: where 17% of them believe that expansion into almost every industry will fragment the imaging market, due in part to industrial use of consumer devices. Also, twenty-one percent (21%) feel that their business could be severely impacted by users who develop and build their own unique cameras and systems.

Overall, the status of machine vision as a standalone discipline is on the decline as it becomes more of an embedded component to a more complete solution. Forty-three percent (43%) of users are currently using embedded vision as part of their integrated automation and control systems. Despite a predicted increase in market growth, some manufacturers were skeptical of this: though users are not about to defect en masse to the Asian market, 59% of manufacturers see competition from this region as a threat.

In addition, 38% are still concerned about the risks relating to embedded vision, like industrial cameras being replaced by specific embedded solutions, as well as changes to traditional business models. Because of the growth and ongoing development of machine vision technologies, the classical roles for manufacturers, integrators, and users are evolving and being constantly challenged.

Embedded vision and the use of imaging technology in nearly every industry points to fragmentation. Users need and want specific solutions for their integrated systems and OEM solutions. This scenario is an opportunity for consulting distributors and system integrators to demonstrate their role as both advisors and partners in the development and implementation of individual and modular embedded vision solutions, far removed from the traditional industrial camera.

Healthy Price Levels, Matrix Cameras, and Global Brand Awareness

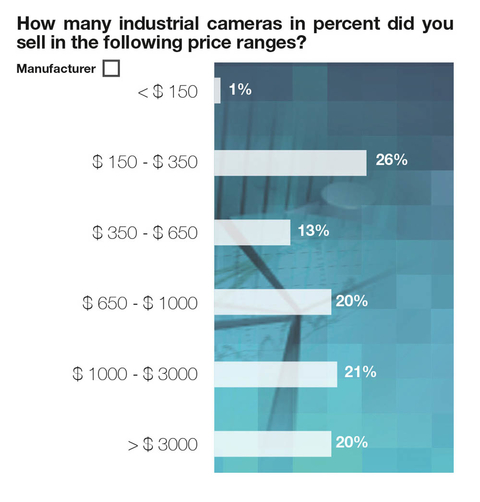

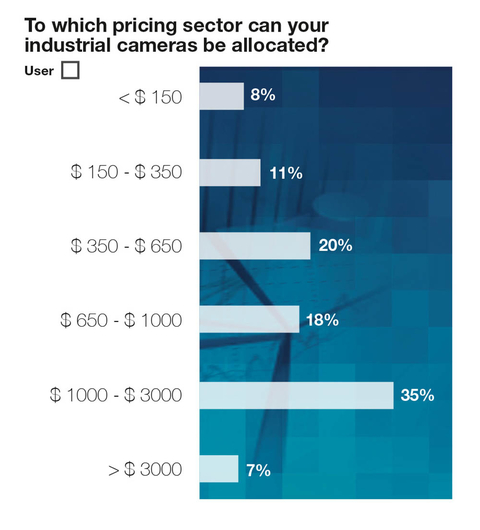

Besides the inherent desire for users to purchase cameras, the price range of these cameras is a key market development indicator. After a gradual decline in prices prior to and including 2015, the cost of mid- and high-price cameras is noticeably more stable in 2017, which should lessen manufacturers' concerns about low cost Asian competition (See Chart 3).

Only 19% of users limited their budget to $350 for a camera, compared to 45% in 2016. Users paying between $350 and $1,000 (38%), or more than $1000 (42%) increased as compared to last year (+7 and +19 percentage points, respectively). The high price segment is clearly growing because more performance is now being added to higher priced cameras. User trends are largely confirmed by manufacturers, especially in terms of a decrease in demand for cameras priced below $150, and the steep increase for those over $1,000 (See Chart 4).

Market fragmentation, embedded vision and highly specific modular vision systems also appear to be promoting quality awareness. Superior image quality with improved processing performance combined with integrated intelligence, speed, and simple connectivity, are key criteria for "smart" investments with good price-performance ratios.

In the 2017 study, demand was mainly for the type of cameras used in vision systems. Area scan cameras, at 60%, are, by far, the users' top choice followed by 3D and stereo vision cameras (8%), and OEM camera modules (8%). Twelve percent (12%) of users utilize a custom designed camera to solve their imaging problems. Seven percent (7%) use line scan cameras and only 5% use smart cameras – representing a sharp decline for smart cameras compared to 27% in 2016.

A significant proportion of those who have changed their usage of smart cameras are likely now using area scan cameras. These cameras, like smart cameras, can be equipped with all the necessary features in a compact form. The view among manufacturers is more balanced: 37% sell area scan cameras, followed by 18% for 3D and stereo vision, 16% for smart cameras, and 10% for OEM modules. However, 16% sell cameras for various special solutions, which clearly plays a key role in their revenues.

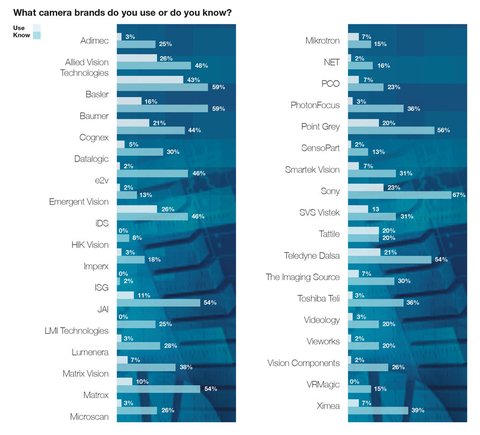

The camera brand best known to users is Sony, with 67% brand awareness – no doubt influenced by its reputation as a high-quality sensor provider and its many consumer products in various segments. Basler and Baumer, each with 59%, and Flir (former Point Grey) with 56%, are all vying for second place behind the top brand. Among users, 54% are familiar with Matrox, Teledyne Dalsa and JAI. However, when it comes to actual use, Basler is the most popular brand (43%), followed by Allied Vision and iDS (26% each); then, Cognex, Sony and Teledyne Dalsa follow with 21% each (See Chart 5).

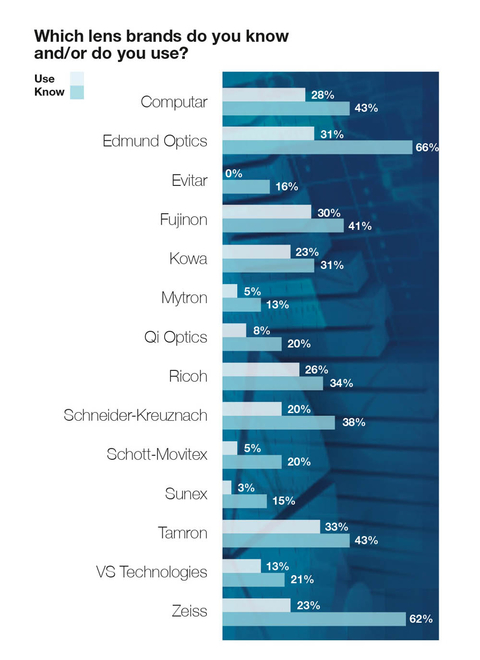

In conjunction with cameras, optics is an important part of any vision systems. The best known optical brand is Edmund Optics at 66%, higher than Zeiss, at 62%. Whether this is due to in-house Edmund lenses, or a familiarity of the distributor’s name with users is not clear from the results. Computar and Tamron share third place in user brand awareness at 43%. However, when it comes to actual usage, Tamron lenses are employed by 33% of users – more than any other brand – followed by Edmund Optics and Fujinon at 31% and 30%, respectively (See Chart 6).

CMOS is the New Norm, Sony and On Semi Remain Popular, and Customized Sensors Gain Momentum

The previously announced decline of the CCD sensor usage is more evident as the switch to CMOS sensors is nearly complete: today, 73% of manufacturers and users employ CMOS technology, while the remaining 27% are still using CCD. This has been accelerated by Sony's discontinuation of CCD technology. The study predicts that CCD usage will fall to 22% among manufacturers and 12% among users – a clear confirmation of recent forecasts and changes in the sensor market landscape.

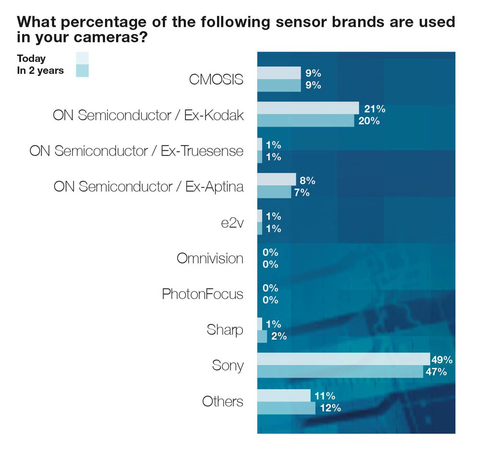

After the groundbreaking technological innovations and resulting upheavals in recent years, the sensor market is showing signs of stabilization. Sony remains the clear market leader with 49% of users, and lost only 4 percentage points compared with 2016. ON Semiconductor’s share changed little at 30%, and the projected 175% growth over last year in customized sensors, increasing their market share to 11%, has been achieved. At 9%, CMOSIS still plays a significant role for users in a clearly segmented sensor market (See Chart 7).

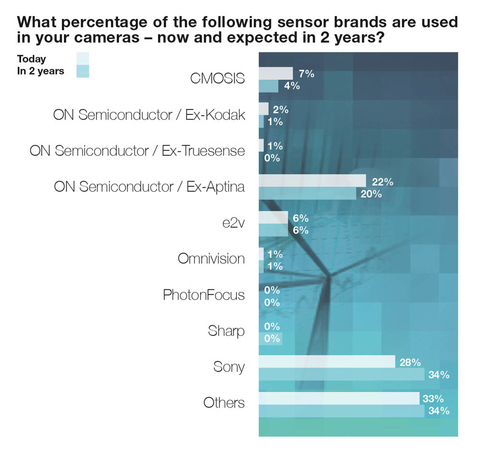

Manufacturers are still fiercely loyal to Sony, with percentages like those from 2016. Although Japan's top dog leads the market at 28%, in-house development is a serious threat to traditional suppliers. According to manufacturers, 33% of their cameras are currently using customized sensors. ON Semiconductor has a 25% market share, almost bringing it level with Sony. Meanwhile, CMOSIS, holds on to its 7% market share. It is clear that camera manufacturers desire themselves to be far more independent of major suppliers and their potential limitations. Customized sensors allow manufacturers to respond more effectively to individual customer requirements, and those requirements for specific embedded vision components (See Chart 8).

Chart 8: Sensor brand usage, manufacturers

Innovative and Groundbreaking at the Same Time: It's All About the Application Area

What criteria are important to users and manufacturers when it comes to selecting and using a specific sensor? CMOS sensors are the new industry standard coming with high quality for those more demanding vision applications. The new market potential in VR/AR, autonomous vehicles and aircraft, intelligent automation and robotics solutions require high sensitivity and high quality for real-time processing and control.

On the other hand, the traditional machine vision market still uses lower resolutions, monochrome sensors, and lower frame rates. These are perfectly sufficient for classic measurement and testing, like when it comes to inspecting the fill level inside a bottle on a conveyor belt traveling at 2m per second, little more is required for automated quality inspection.

The breakdown of the required criteria by application is clear from the survey data on technical sensors. Looking at sensor resolution first, the main category being used is between 1 to 3 megapixels and comes in at 40%. Although this figure represents a decrease of 15 percentage points from 2016, users expect this category to remain stable over the next two years.

Last year's smallest usage category, that of sensors with less than 1 megapixel, made a modest gain of 22%. Meanwhile, the high-resolution category, the one between 10 and 20 megapixels, increased significantly. Based on the feedback received, combined with the increased use of innovation-driven vision applications, manufacturers reported a decrease in all sensor categories under 5 megapixels but was offset by a rise in all those over 5 megapixels.

While the 1- to 3-megapixel range remains in the lead at 24%, the sensors forecasted to grow most significantly are those in the 5 to 10 megapixels range, and 10 and 20 megapixels range, at 88% and 67% respectively. However, in traditional machine vision, stable manufacturer forecasts for VGA resolution show that it remains an important component of their sales.

With sensor image formats, a little more than two-thirds of users prefer a 1/3- to 2/3-inch sensor format, while one-third (33%) of users use a 1/2 inch and a 2/3-inch sensor format. This result is a clear shift toward the higher format category compared to last year, and is probably driven by increasing requirements for image and analysis quality.

Despite big advances in miniaturization of sensors and their respected pixel sizes while still providing equal or even improved performance over previous generations, bigger pixel sizes ensure better utilization of incidental light. Sensors used by manufacturers varies widely by application area: 35% use very large sensors over 1 inch, and 27% use small sensors from 1/2 to 1/3 inch.

Also, manufacturers are increasingly implementing color sensors in their designs, though most users (76%) are still working with monochrome (versus 24% color). C-mount lenses, at 45% (users) and 46% (manufacturers), are the dominant lens type, with a strong tendency toward custom solutions. Manufacturers categorized 34% of versions as "Other" (special solutions) for their lens mount of choice, but 19% of users also specified this category when asked the same question. A significant majority of users seek global shutters as an on-sensor readout technology, thereby benefiting from excellent image quality without motion blur, especially in fast moving applications.

High Image Frame Rates and High Bandwidths are Making Real-Time Processing Feasible

The demand for high speed imaging systems for data analysis and control in real-time is driving developments in image frame rates and data transmission standards. Here too, the split between moderate-speed traditional machine vision systems and innovative high-speed applications is marked. The use of cameras below 25 frames per second (fps) recovered significantly at 51% this year, while there was a corresponding decrease in last year's main category, that being the 25 to 60 fps group. However, applications using devices running at 60 to 100 fps doubled from 7% to 14% in this year’s study.

Manufacturers report that image rates between 25 and 60 fps are still their bestsellers, and are forecasting robust growth in their high-speed product lines: 60 to 100 fps (+53%), 100 to 200 fps (+67%) and over 200 fps (+21%). This growth is a clear signal that users are looking for faster speeds from their imaging products (See Chart 9).

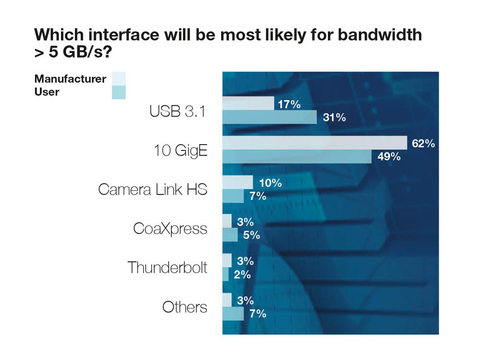

Despite the difference in user and manufacturer responses about image rate requirements, almost 50% of users view transmission rates of more than 5 gigabits per second as relevant or very relevant to their applications, which is expected to rise more than 70% over the next two years. Real-time monitoring and analysis is one of the key benefits and is a driver for continued development when it comes to vision technology expansion. Fast image rates and rapid transmission of the data for immediate processing are a must for high-precision applications. Users are recognizing this potential thus see the logical conclusion as a shift toward higher speeds (See Chart 10).

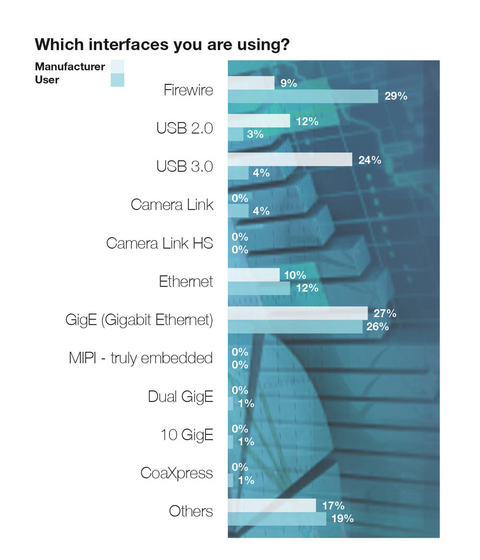

When it comes to data interfaces for imaging systems, GigE Vision is the most accepted transmission standard among manufacturers and users, at 27% and 26%, respectively. FireWire and CoaxPress gained ground compared against the 2016 poll, but this might be a result of a different respondent mix in this year’s study.

Where future high-speed interfaces are concerned, users (at 48%) and manufacturers (at 62%) agree: 10GigE is going to be used to quickly transmit high data volumes in the near term. The ongoing development of the GigE Vision standard predicts a simple upgrade and straightforward connectivity, without additional components. Frame grabbers, despite a decrease of about 10%, retain their position and their justification for specific applications: more than a fifth (+20%) of both manufacturers and users employ them and plan to continue into 2019.

A Steady Trend: Precision, High Performance and Efficiency, Plus Ease-of-Use

“As always, the comments received are the most interesting aspect”, says survey sponsor and FRAMOS CEO Dr. Andreas Franz. “Alongside the purely technical survey data, these comments give us a completely unfiltered view of what participants expect from the imaging market and what kind of developments they are predicting. Since the survey guarantees anonymity, both manufacturers and users gave very revealing answers on their feel for the market and forthcoming changes.”

In an era of zero-error production of systems starting at a small batch size of 1, many users emphasize the importance of greater precision in automation, measurement, and testing. They expect to achieve this goal through improved vision performance using higher resolutions, better sensor technologies, and high image frame and transmission rates to retrieve and consume this data very rapidly.

At the same time, higher performance must come in at lower costs and at better price-performance ratios to make it viable for them to implement it into their systems. In particular, smaller operators along with new application markets are looking to capitalize on this improvement in efficiency but profitability and ROI (return on investment) are major factors across the board in their decision process. Participants, as in last year's study, stated that imaging must have a clear benefit for them but also needs to keep them profitable.

The conditions for further growth are still the same this year according to users who also stated a need for easy system integration and straightforward component assembly. User-friendliness, open source software and libraries, intelligent algorithms, and consistent interfaces are a must for most users to allow for ongoing growth in imaging.

These results come as no surprise considering the most recent vision system customizations and more frequent in-house implementations. Also, users expect the whole vision system to be supported by data security and wireless connections. Users want to expand the potential of their imaging applications with more analysis options, while maintaining and improving on quality assurance and significant production optimization.

Along with Smart Factory optimization and traditional machine vision, users see huge potential in embedded vision technologies for 3D applications and in deep learning using artificial intelligence. The imaging landscape, given the exhaustive application potential of sensors, has an opportunity to conquer and revolutionize new industries where most users are still deliberating over specific applications. This is a big opportunity for system integrators and value add distributors to generate new custom solutions with practical examples and use cases, and to increase the market penetration of imaging systems.

Artificial Intelligence, Human-Machine Teamwork and Innovative Applications

Manufacturers agree with users on the following points: they are looking for higher performance at lower prices from vision technologies, and they want good usability and consistent interfaces. Manufacturers make it very clear that quality is a top priority, both in terms of differentiating themselves from Asian competitors, and to gain a solid foothold in new markets with more demanding requirements.

Consequently, alongside increased automation and the Smart Factory, manufacturers have a far greater focus for using artificial intelligence. In their view, human-machine collaboration, specifically in robotics, and an increasing number of autonomous driving and aviation systems are key areas of growth. The new imaging solutions from Intel and Nvidia, who have capitalized on their processing expertise to produce innovative, cognitive vision systems, were frequently mentioned in manufacturers’ comments. They believe the entire imaging industry will reap the benefits of this innovation.

One obvious conclusion is that it will drive expansion into new industries, and into more consumer segments. Demands for standardization should help mitigate the resulting fragmentation and customization often seen with new technology introductions.

Conclusion

The results of the FRAMOS 2017 Market Study clearly indicate that imaging is no longer a standalone discipline, but is increasingly an integral part of modern automation and control systems. Along with traditional machine vision applications, embedded vision now provides the capability to analyze images at lightning speed and to make independent decisions based on the captured visual data.

The real growth potential of vision technology rests on increased penetration into the Smart Factory, together with the innovative use of artificial intelligence in new industries and consumer markets. Visual sensor technology is equipping machines with human senses and human intelligence, giving them the capability to “sense”, understand, interact, and learn. New types of consumer goods, safety features, and industrial solutions are becoming viable thanks to reliable wireless devices like those used for eye-tracking, gesture, and face recognition.

Self-aware robots, collision avoiding drones, and reliable monitoring solutions are just a few examples that are expected to be seen in industry. Now, smart homes can be controlled with a swipe of a finger, and cars can automatically brake if they detect the driver falling asleep at the wheel. Imaging is becoming a fundamental building block of the digitally networked world and is contributing to greater efficiency, security and comfort in every area of life.

For more details about the study and/or products, contact FRAMOS Technologies Inc.,

Ottawa, Ontario, Canada. 613-208-1082 / 613-686-1152 or email [email protected]